Debt is a common part of many people’s financial lives, but it doesn’t have to control your future. Managing your debt effectively and paying it off faster can bring you peace of mind and help you achieve your financial goals. Whether you have credit card debt, student loans, or a mortgage, taking steps to pay down your debt can help you get on a path toward financial freedom.

In this article, we will discuss how to manage your debt, create a strategy for paying it off faster, and avoid falling back into debt.

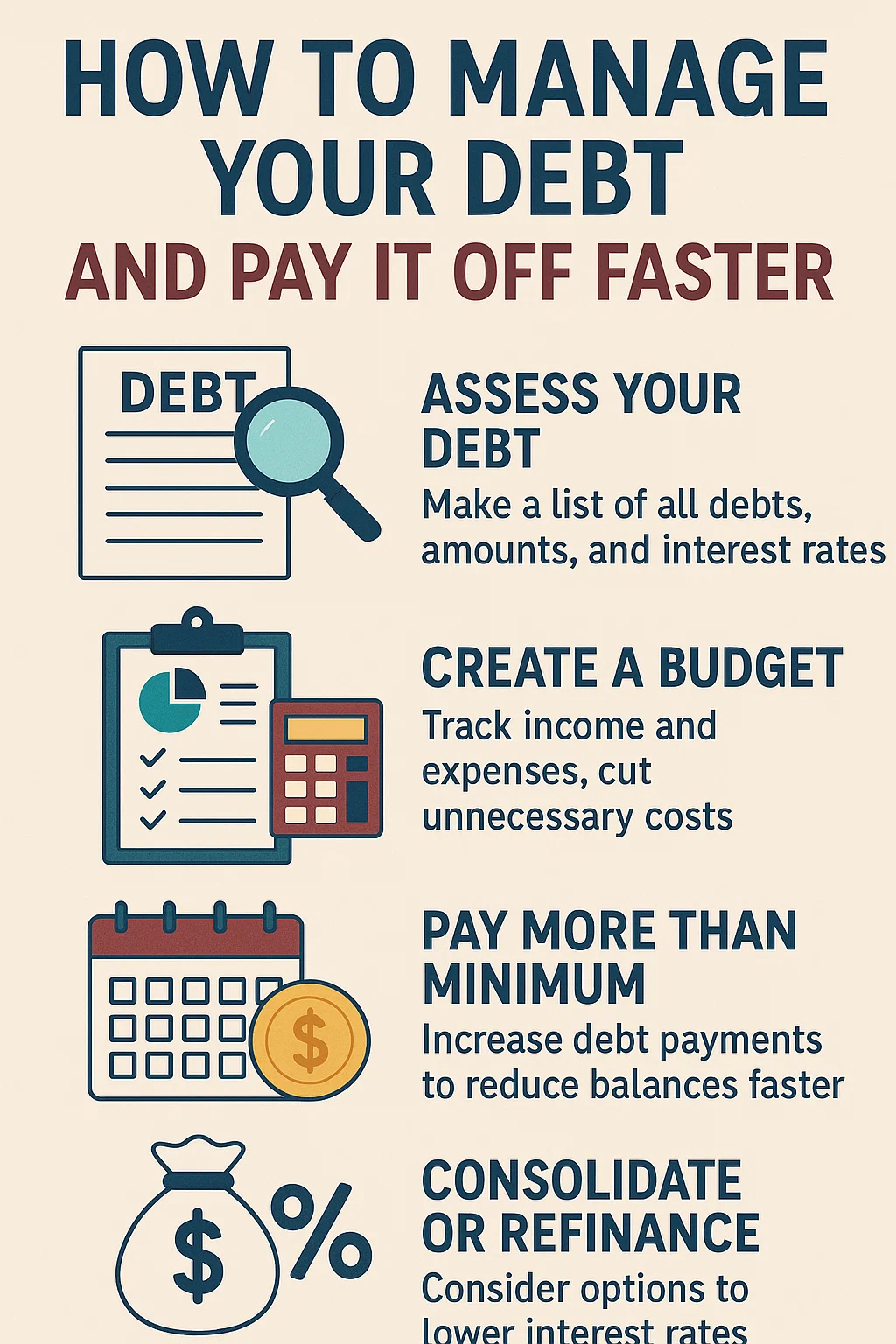

1. Understand Your Debt

The first step in managing your debt is understanding exactly how much you owe and to whom. This will give you a clear picture of your financial situation and help you create a plan to pay off your debt.

Steps to Understand Your Debt:

- List All Your Debts: Make a list of every debt you owe, including credit cards, student loans, car loans, mortgages, and personal loans.

- Record Interest Rates: Note the interest rates for each of your debts. High-interest debt, such as credit cards, should be prioritized over low-interest debt.

- Identify Minimum Payments: Make a note of the minimum payments required for each debt. This will help you understand how much you need to pay each month to avoid penalties.

Having a clear view of your debt will help you create a strategy for paying it off.

2. Prioritize High-Interest Debt

When you have multiple debts, it’s essential to prioritize paying off the high-interest debt first. High-interest debt, such as credit cards, can quickly accumulate, making it harder to pay off your other debts.

How to Prioritize Debt:

- The Debt Avalanche Method: This method focuses on paying off the debt with the highest interest rate first. While it may take longer to pay off individual debts, this approach saves you the most money over time because you’re minimizing the amount of interest you pay.

- The Debt Snowball Method: With the debt snowball method, you focus on paying off the smallest debt first, while continuing to make minimum payments on other debts. This method provides a psychological boost as you see debts disappearing, which can motivate you to keep going.

Example of Debt Prioritization:

If you have the following debts:

- Credit card: $5,000 balance with a 20% interest rate

- Student loan: $10,000 balance with a 5% interest rate

With the debt avalanche method, you would focus on paying off the credit card first because of its high-interest rate. Once the credit card is paid off, you would move on to the student loan.

3. Create a Debt Repayment Plan

Now that you’ve prioritized your debts, it’s time to create a debt repayment plan. A plan helps you stay organized and ensures that you are making consistent progress toward becoming debt-free.

How to Create a Debt Repayment Plan:

- Set a Budget: Create a budget that accounts for your income and all of your expenses, including debt payments. Make sure to allocate as much as possible toward paying off your debt.

- Determine How Much Extra to Pay: Identify how much extra money you can put toward paying off your debts each month. This could come from cutting back on discretionary spending or finding ways to increase your income.

- Set a Timeline: Set a timeline for paying off each debt. For example, if you want to pay off your credit card in 12 months, determine how much you need to pay each month to achieve that goal.

4. Make Extra Payments Whenever Possible

One of the most effective ways to pay off debt faster is to make extra payments whenever possible. If you can afford to pay more than the minimum required amount, do it. Extra payments reduce the principal balance, which in turn reduces the amount of interest you will pay over time.

Ways to Make Extra Payments:

- Windfalls: Use unexpected income, such as tax refunds, bonuses, or gifts, to make additional payments toward your debt.

- Side Income: Consider earning extra money through a side hustle or freelance work and putting that money toward paying off your debt.

- Round-Up Payments: Some financial apps allow you to round up purchases to the nearest dollar and automatically apply the difference to your debt.

5. Avoid Accumulating More Debt

One of the biggest mistakes people make when trying to pay off debt is accumulating more debt while working to eliminate existing balances. Avoid using credit cards or taking out new loans while you’re paying off debt.

Tips to Avoid Accumulating More Debt:

- Freeze Your Credit Cards: Consider freezing your credit cards to avoid the temptation to use them while you’re paying off existing debt.

- Use Cash or Debit: Pay with cash or debit instead of credit to avoid accumulating new debt.

- Build an Emergency Fund: Having an emergency fund will help you avoid relying on credit cards for unexpected expenses. Aim to save at least three to six months’ worth of living expenses in a separate savings account.

6. Consider Debt Consolidation

If you have multiple high-interest debts, debt consolidation might be a good option to simplify your payments and potentially reduce your interest rate. Debt consolidation involves combining multiple debts into one loan, often with a lower interest rate.

Debt Consolidation Options:

- Balance Transfer Credit Cards: Some credit cards offer 0% introductory APR on balance transfers for a set period, allowing you to pay off your debt without accruing interest for several months.

- Personal Loans: A personal loan can be used to pay off high-interest credit card debt. Look for a loan with a lower interest rate than your current debts.

- Home Equity Loans: If you own a home, you might be able to consolidate debt through a home equity loan, which typically offers a lower interest rate than credit cards.

Risks of Debt Consolidation:

While debt consolidation can simplify your payments and reduce interest rates, it’s important to avoid accumulating new debt while consolidating. Be sure to maintain discipline and stick to your repayment plan.

7. Monitor Your Progress and Stay Motivated

Staying motivated and tracking your progress is crucial in your journey to become debt-free. Regularly checking in on your progress can help you stay on track and celebrate small milestones along the way.

Ways to Track Progress:

- Track Your Debt Reduction: Monitor how much you’ve paid off and how much you have left. Celebrate when you reach milestones, such as paying off 25%, 50%, or 75% of your debt.

- Use Debt Tracking Apps: There are several apps available that allow you to track your debt repayment progress, such as Debt Payoff Planner or Undebt.it.

- Stay Positive: It can take time to pay off debt, but remember that every payment brings you one step closer to financial freedom. Stay focused on your goal and remind yourself why you’re doing this.

8. Seek Professional Help if Necessary

If you’re feeling overwhelmed by debt, seeking professional help can be a smart option. Credit counseling services can help you create a debt repayment plan, negotiate with creditors, and provide guidance on managing your finances.

How a Credit Counselor Can Help:

- Debt Management Plans (DMP): A credit counselor can work with you to create a DMP, which consolidates your debts into one payment and may reduce interest rates or waive fees.

- Negotiation: Counselors can negotiate with creditors on your behalf to potentially lower your monthly payments or interest rates.

- Financial Education: Credit counselors can provide financial education to help you avoid falling into debt in the future.

Be sure to choose a reputable, nonprofit credit counseling agency to avoid predatory companies.

Conclusion: Take Control of Your Debt

Managing and paying off debt can feel like an uphill battle, but with the right strategy and a disciplined approach, you can regain control of your finances and achieve your goal of becoming debt-free. Whether you use the debt avalanche or snowball method, make extra payments, or seek professional help, the key is to stay consistent and committed to your plan.

With patience and perseverance, you’ll find that paying off your debt is not only possible but also incredibly rewarding. Start today, and take the first step toward a debt-free future.