Unexpected expenses can derail your entire financial plan if you’re not prepared. Whether it’s a car repair, a medical bill, or losing your job, life has a way of throwing surprises your way. That’s why building an emergency fund is one of the most important first steps in managing your personal finances. In this guide, you’ll learn what an emergency fund is, why it matters, how much you should save, and how to start building one today — even if you’re on a tight budget.

What Is an Emergency Fund?

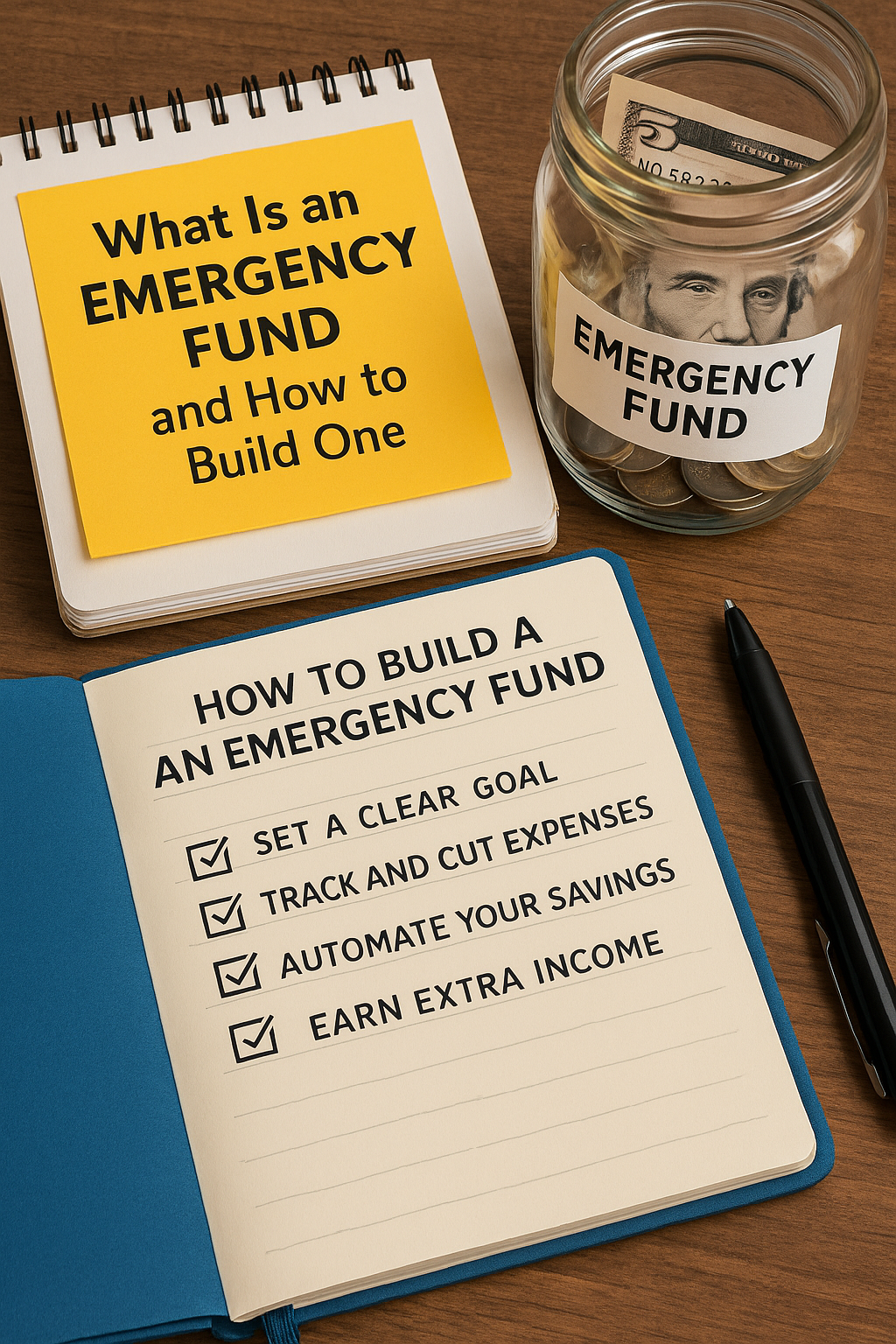

An emergency fund is a dedicated amount of money set aside to cover unforeseen expenses or financial emergencies. It’s not for vacations, impulse purchases, or even planned expenses like rent or a new phone. It’s your financial safety net — money you can access quickly without going into debt.

Why You Need an Emergency Fund

Without an emergency fund, even a small unexpected expense can throw off your entire budget. Here are a few reasons why it’s essential:

- Prevents debt accumulation: You won’t need to rely on credit cards or loans in a crisis.

- Provides peace of mind: Knowing you have a buffer reduces anxiety.

- Improves financial stability: You can recover faster from setbacks.

- Gives you time: If you lose your job, the emergency fund buys you time to find another without panicking.

How Much Should You Save?

The ideal amount for an emergency fund depends on your lifestyle, obligations, and risk tolerance. A common rule of thumb is:

- Beginner level: Start with $500 to $1,000 to cover small emergencies.

- Stable level: Save enough to cover 3 to 6 months of essential expenses — rent, food, utilities, insurance, and minimum debt payments.

If you’re self-employed, have a family, or your income is irregular, consider saving even more. The goal is to be able to live without income for several months without going into debt.

Where to Keep Your Emergency Fund

Your emergency fund should be:

- Safe: Avoid risky investments.

- Accessible: You should be able to withdraw the money quickly.

- Separate: Keep it in a different account to avoid the temptation of spending.

The best options include:

- High-yield savings accounts

- Money market accounts

- Certificates of deposit (CDs) (only if you can access them without penalties)

Avoid using regular checking accounts or long-term investment platforms like stocks or retirement accounts for this purpose.

How to Start Building Your Emergency Fund

1. Set a Clear Goal

Start with a realistic goal. If you can’t save three months of expenses immediately, aim for $500, then $1,000. Break it down into weekly or monthly savings targets to stay motivated.

2. Track and Cut Expenses

Review your monthly expenses to find areas where you can cut back. Even small changes can make a difference:

- Cancel unused subscriptions

- Cook more meals at home

- Reduce takeout or delivery

- Buy in bulk for essentials

- Use public transportation or carpool

Redirect those savings directly into your emergency fund.

3. Automate Your Savings

Set up automatic transfers from your checking to your emergency savings account. Treat this as a non-negotiable bill that gets paid every month. Even $25 per week adds up over time.

4. Use Windfalls Wisely

Tax returns, work bonuses, or unexpected gifts of money are great opportunities to boost your emergency fund. Instead of spending that cash, allocate at least part of it to your savings.

5. Sell Unused Items

Decluttering can turn into dollars. Sell unused electronics, clothes, or furniture online and add the proceeds to your emergency fund.

6. Earn Extra Income

If your budget is too tight, consider a side hustle. Freelance work, tutoring, pet sitting, or rideshare driving can generate additional income. Channel those earnings into your fund.

When Should You Use Your Emergency Fund?

This money should only be used for genuine emergencies. Ask yourself:

- Is it unexpected?

- Is it urgent?

- Is it necessary?

Examples of valid reasons to use the emergency fund:

- Emergency medical expenses

- Essential car repairs

- Sudden job loss

- Urgent home maintenance (like a burst pipe)

Not valid: vacation, new gadgets, shopping sprees, or anything that can be planned or postponed.

Rebuilding After Using Your Fund

If you’ve dipped into your emergency fund, prioritize rebuilding it as soon as possible. Pause other savings or non-essential spending temporarily and redirect funds to bring your emergency reserve back to its full amount.

Building Confidence and Security

Starting an emergency fund, especially when money is tight, can feel slow and frustrating. But remember — even small steps make a big difference over time. The peace of mind that comes with knowing you’re prepared for the unexpected is worth every sacrifice.

Commit to your savings goal today and take control of your financial future.